Hello ,

I am facing some issues with Preprocessing. When I a running the section with preprocessing this is what I get:

AttributeError: module 'sklearn.preprocessing' has no attribute 'new_dataset'

Here is the code of yours. Am I missing any steps?

#Edit Author: Ray

IMPORTING IMPORTANT LIBRARIES

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

import math

from sklearn.preprocessing import MinMaxScaler

from sklearn.metrics import mean_squared_error

from keras.models import Sequential

from keras.layers import Dense, Activation

from keras.layers import LSTM

from sklearn import preprocessing # how to import preprocessing

import sklearn.preprocessing

import numpy as np

FOR REPRODUCIBILITY

np.random.seed(7)

IMPORTING DATASET

dataset = pd.read_csv('C:/Users/ray/Documents/Python Scripts/LSTM-Stock-prediction-master/apple_share_price.csv', usecols=[1,2,3,4])

dataset = dataset.reindex(index = dataset.index[::-1])

CREATING OWN INDEX FOR FLEXIBILITY

obs = np.arange(1, len(dataset) + 1, 1)

TAKING DIFFERENT INDICATORS FOR PREDICTION

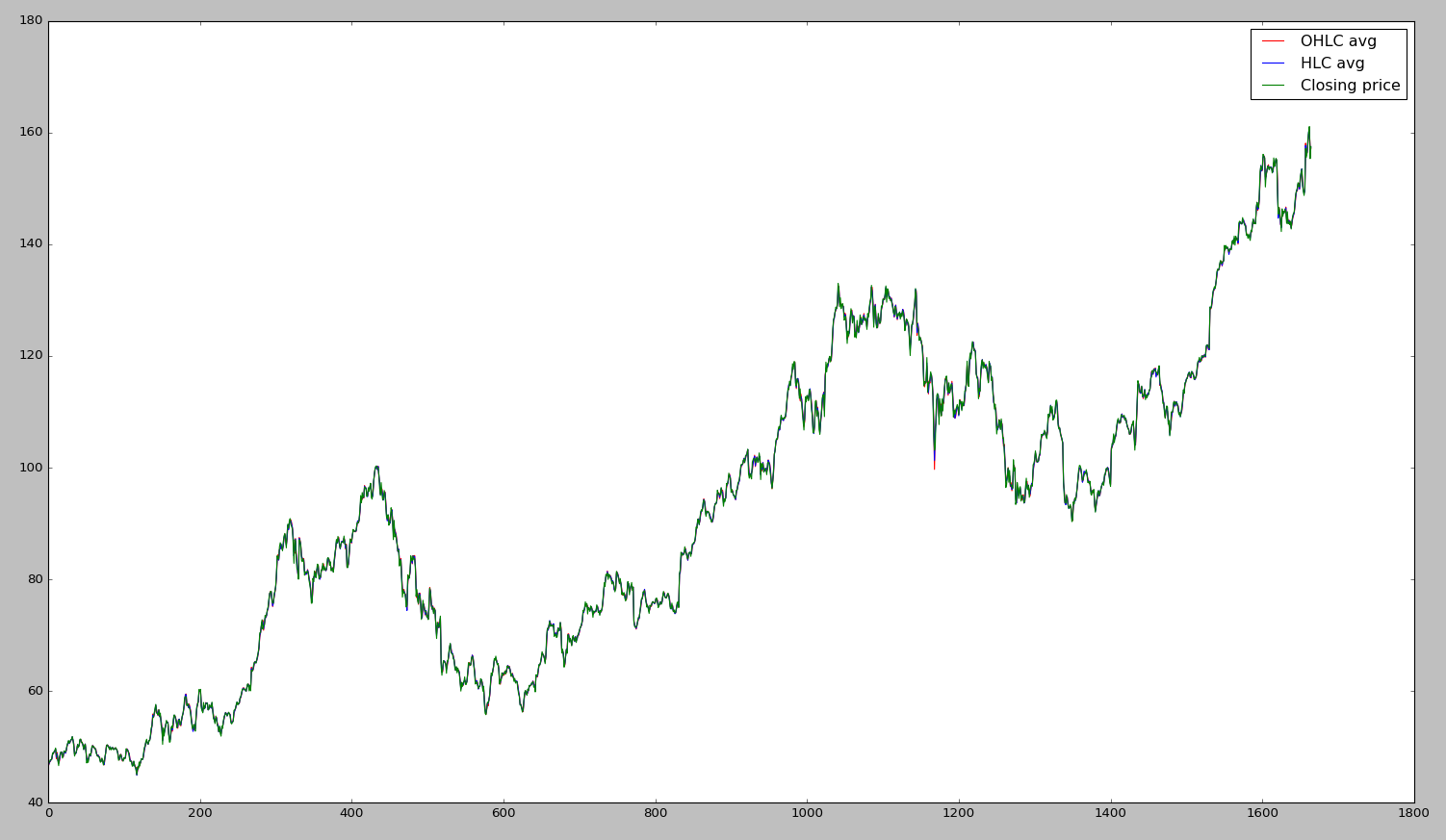

OHLC_avg = dataset.mean(axis = 1)

HLC_avg = dataset[['High', 'Low', 'Close']].mean(axis = 1)

close_val = dataset[['Close']]

PLOTTING ALL INDICATORS IN ONE PLOT

plt.plot(obs, OHLC_avg, 'r', label = 'OHLC avg')

plt.plot(obs, HLC_avg, 'b', label = 'HLC avg')

plt.plot(obs, close_val, 'g', label = 'Closing price')

plt.legend(loc = 'upper right')

plt.show()

PREPARATION OF TIME SERIES DATASET

OHLC_avg = np.reshape(OHLC_avg.values, (len(OHLC_avg),1)) # 1664

scaler = MinMaxScaler(feature_range=(0, 1))

OHLC_avg = scaler.fit_transform(OHLC_avg)

TRAIN-TEST SPLIT

train_OHLC = int(len(OHLC_avg) * 0.75)

test_OHLC = len(OHLC_avg) - train_OHLC

train_OHLC, test_OHLC = OHLC_avg[0:train_OHLC,:], OHLC_avg[train_OHLC:len(OHLC_avg),:]

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

step_size = 1

FUNCTION TO CREATE 1D DATA INTO TIME SERIES DATASET

def new_dataset(dataset, step_size):

trainX, trainY = [], []

for i in range(len(dataset)-step_size-1):

a = dataset[i:(i+step_size), 0]

trainX.append(a)

trainY.append(dataset[i + step_size, 0])

return np.array(trainX), np.array(trainY)

TIME-SERIES DATASET (FOR TIME T, VALUES FOR TIME T+1)

trainX, trainY = sklearn.preprocessing.new_dataset(train_OHLC, 1)

testX, testY = sklearn.preprocessing.new_dataset(test_OHLC, 1)

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

RESHAPING TRAIN AND TEST DATA

trainX = np.reshape(train_OHLC, (train_OHLC.shape[0], 1, train_OHLC.shape[1]))

testX = np.reshape(testX, (testX.shape[0], 1, testX.shape[1]))

step_size = 1

LSTM MODEL

model = Sequential()

model.add(LSTM(32, input_shape=(1, step_size), return_sequences = True))

model.add(LSTM(16))

model.add(Dense(1))

model.add(Activation('linear'))

MODEL COMPILING AND TRAINING

model.compile(loss='mean_squared_error', optimizer='adagrad') # Try SGD, adam, adagrad and compare!!!

model.fit(trainX, trainY, epochs=5, batch_size=1, verbose=2)

PREDICTION

trainPredict = model.predict(trainX)

testPredict = model.predict(testX)

DE-NORMALIZING FOR PLOTTING

trainPredict = scaler.inverse_transform(trainPredict)

trainY = scaler.inverse_transform([trainY])

testPredict = scaler.inverse_transform(testPredict)

testY = scaler.inverse_transform([testY])

TRAINING RMSE

trainScore = math.sqrt(mean_squared_error(trainY[0], trainPredict[:,0]))

print('Train RMSE: %.2f' % (trainScore))

TEST RMSE

testScore = math.sqrt(mean_squared_error(testY[0], testPredict[:,0]))

print('Test RMSE: %.2f' % (testScore))

CREATING SIMILAR DATASET TO PLOT TRAINING PREDICTIONS

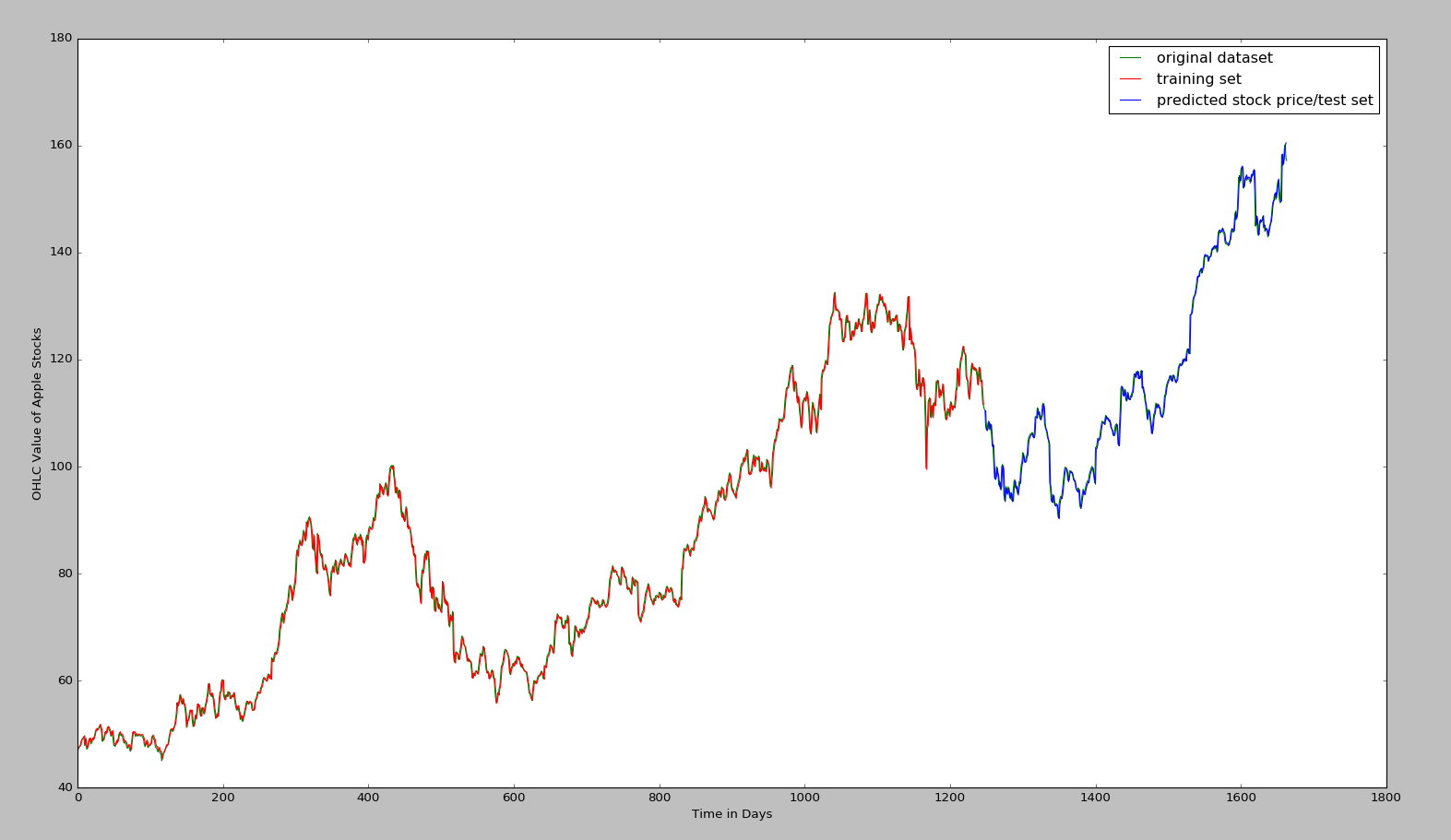

trainPredictPlot = np.empty_like(OHLC_avg)

trainPredictPlot[:, :] = np.nan

trainPredictPlot[step_size:len(trainPredict)+step_size, :] = trainPredict

CREATING SIMILAR DATASSET TO PLOT TEST PREDICTIONS

testPredictPlot = np.empty_like(OHLC_avg)

testPredictPlot[:, :] = np.nan

testPredictPlot[len(trainPredict)+(step_size*2)+1:len(OHLC_avg)-1, :] = testPredict

DE-NORMALIZING MAIN DATASET

OHLC_avg = scaler.inverse_transform(OHLC_avg)

PLOT OF MAIN OHLC VALUES, TRAIN PREDICTIONS AND TEST PREDICTIONS

plt.plot(OHLC_avg, 'g', label = 'original dataset')

plt.plot(trainPredictPlot, 'r', label = 'training set')

plt.plot(testPredictPlot, 'b', label = 'predicted stock price/test set')

plt.legend(loc = 'upper right')

plt.xlabel('Time in Days')

plt.ylabel('OHLC Value of Apple Stocks')

plt.show()

PREDICT FUTURE VALUES

last_val = testPredict[-1]

last_val_scaled = last_val/last_val

next_val = model.predict(np.reshape(last_val_scaled, (1,1,1)))

print "Last Day Value:", np.asscalar(last_val)

print "Next Day Value:", np.asscalar(last_val*next_val)

print np.append(last_val, next_val)

please fix me if i wrong

please fix me if i wrong

1.3k Dec 28, 2022

1.3k Dec 28, 2022

26 May 26, 2022

26 May 26, 2022

39 Nov 21, 2022

39 Nov 21, 2022

15 Aug 20, 2022

15 Aug 20, 2022

2 Dec 13, 2022

2 Dec 13, 2022

116 Nov 9, 2022

116 Nov 9, 2022

69 Dec 26, 2022

69 Dec 26, 2022

1 Jun 13, 2022

1 Jun 13, 2022

84 Jan 1, 2023

84 Jan 1, 2023

251 Dec 17, 2022

251 Dec 17, 2022

194 Dec 28, 2022

194 Dec 28, 2022

2 Jan 30, 2022

2 Jan 30, 2022

1 Nov 20, 2021

1 Nov 20, 2021

318 Dec 14, 2022

318 Dec 14, 2022

1 Oct 29, 2021

1 Oct 29, 2021

3 Sep 30, 2021

3 Sep 30, 2021

10 Dec 10, 2021

10 Dec 10, 2021

1 Jan 15, 2022

1 Jan 15, 2022

243 Dec 26, 2022

243 Dec 26, 2022